What’s Changing

For two decades federal loans functioned as something close to a guarantee that law school could be financially accessible. Even those facing modest salary outcomes could borrow what they needed, repay on an income-driven schedule, and utilize forgiveness programs to eventually become debt-free.

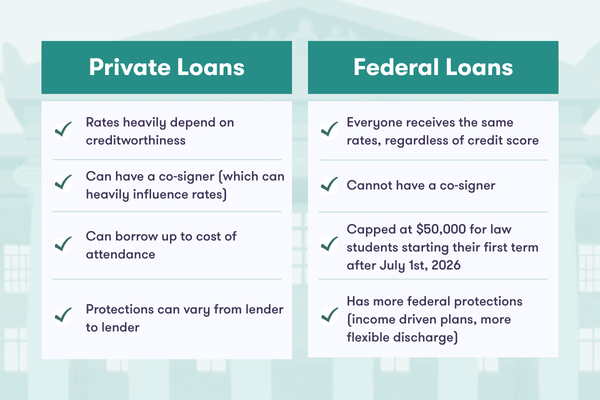

Starting this July, new federal regulations are eliminating the Graduate PLUS loan for new borrowers and cap how much graduate students can borrow through federal loan programs. This will leave many law students with a gap between federal aid and their actual expenses.

Those without family money or significant scholarships are left with private loans as their financing option.

And private lending presents a very different scenario.

Why Private Loans Are Harder to Navigate

Graduate PLUS loans allowed students to borrow up to the full cost of attendance with the barest of credit requirements – something opponents of the program often cited as problematic. Interest rates were fixed at the same levels for every borrower.

Private loan approval and rates heavily depend on the creditworthiness of the borrower. Law students in their early to mid-twenties may struggle to meet minimum credit length requirements even if they have done no damage to their credit. There is going to be an increased need for creditworthy cosigners for borrowers who are unable to secure financing based on their own history.

Given the 20-year availability of the Graduate PLUS loan, the financial education surrounding private loan selection has been missing from the conversation. For instance, many borrowers do not realize that shopping around for a student loan rate is highly advantageous as rate ranges on school lender lists do not give solid information on where a borrower will fall in that range.

According to Experian and MyFICO, multiple student loan applications do not impact your FICO score when applications are completed within a 14-45 day timeframe.

While federal loans all follow the same set of rules and regulations, the terms of a private loan can vary significantly from lender to lender. Borrowers must navigate disclosures carefully to ensure they understand the differences between products.

Here are a few key items to take into consideration when comparing products:

- Interest rate and APR

- Term Length

- Repayment options (deferred, fixed, interest only, full repayment)

- Cosigner release availability (if applicable)

- Death and disability discharge

- Clerkship deferment availability

- Discounts (autopay, graduation, etc.)

Juno’s Group Negotiation Model

Juno was built on a straightforward premise: borrowers negotiating together have leverage that borrowers negotiating alone never will.

Juno isn’t a lender. It’s a collective bargaining group for borrowers.

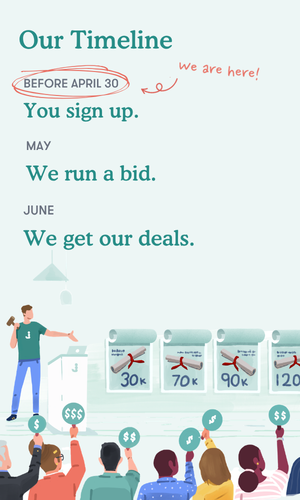

The idea is simple: lenders are often willing to offer better deals to groups than to individuals. From November to May, Juno encourages as many students as possible to sign up for the negotiation group to maximize impact. New deals secured through negotiation are released each June and students can see personalized rates based on their credit score through a soft credit check. Over the past 8 years, Juno has helped its members navigate the process resulting in negotiated group deals to the tune of over $1B in student loans and student loan refinancing.

Joining the group is free, and there’s no obligation to borrow.

Past negotiations have resulted in:

- Discounted rates and exclusive benefits: lenders offered Juno members reduced rates or cash back, making Juno an obvious choice for borrowers.

- Broader eligibility — In 2025, 85% of approved Juno members secured loans without a cosigner, compared to ~20% of the broader market.

- A rate match guarantee: borrowers who found a lower rate through an eligible lender were able to get the rate matched and 1% of their loan value in cash back.

Additionally, Juno is committed to providing strong borrower education. This includes access to resource hubs, live webinars, and free one-on-one meetings with experts.

The Bigger Picture

Federal loans built a degree of equity into the system. Credit (or lack thereof) and family wealth didn’t determine whether you could become a lawyer.

As those protections shrink, there’s a real risk that private lending becomes the new gatekeeper to the legal profession.

Juno’s model doesn’t wait for policy to change. It works within the existing private market to give borrowers more power — and in doing so, helps keep legal education within reach for more people

The information provided in this article is current as of April 1, 2026, and is intended for general informational purposes only. It does not constitute legal, financial, or tax advice. Readers should consult their own advisors before making any decisions. Terms and conditions may apply to the loan products discussed. Federal student loans offer certain borrower protections and benefits—such as income-driven repayment plans and potential forgiveness options—that are important to consider. To learn more, visit studentaid.gov.

Leah Young is the Student Success Resource Lead at Juno. She has nearly 20 years of experience in student financial aid and financial literacy initiatives. Leah served as a Law School Director of Admissions and Financial Aid and was an Accredited Financial Counselor® for a legal education non-profit prior to joining Juno’s efforts to expand quality private loan options post-OBBBA.

The post Keeping Law School Accessible When Federal Loans Fall Short appeared first on Above the Law.